PhoneLoan Offers Instant Digital Loans Up to NPR 5 Lakhs

Kathmandu. How carefully do you look at the information displayed in your bank's mobile banking application? If you don't pay much attention, check it once now. You might see an icon named 'BankLoan' or something similar. This could be very beneficial for you.

This is a system that can give you an instant loan. For this, you don't have to go to any bank branch, nor do you have to pledge any collateral. Without spending a single piece of paper, you can get a loan within one or two minutes through your mobile.

Various banks and financial institutions are meticulously analyzing the behavior of their customers to determine whether that person is eligible for a loan without collateral and, if so, how much loan they are eligible for. 'PhoneLoan' is assisting in this in-depth analysis.

What is PhoneLoan and how much can be obtained?

PhoneLoan is a digital loan program operated under the 'Credit Infrastructure as a Service' platform of PhoneLoan Private Limited. In simple terms, it is a loan directly available through a mobile app from the banking system without any paperwork.

This service is being provided under the digital lending guideline issued by Nepal Rastra Bank. According to Uddhav Sigdel, Head of Risk and Partnership Department at PhoneLoan, under this, a customer can get a personal loan of up to a maximum of NPR 5 lakhs.

'This is a completely paperless and collateral-free facility. This is 100 percent digital lending,' Sigdel says. 'No customer has to go to a bank branch, submit documents, sign, or show collateral. Customers can get a loan of up to NPR 5 lakhs with a tenure of 1 month to 3 years.'

Facility in 10 Commercial Banks, NPR 17 Billion Loan Disbursed

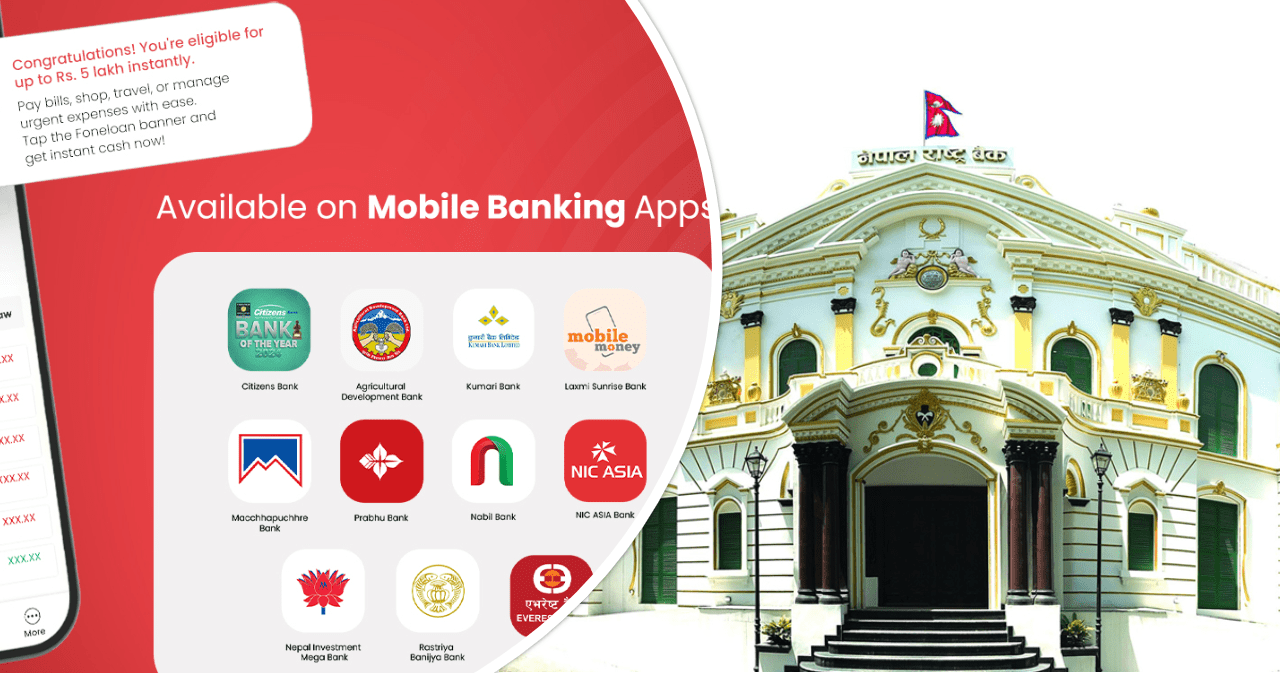

This facility from PhoneLoan is currently being provided by major commercial banks in Nepal. Department Head Sigdel states that 10 commercial banks have been onboarded to the PhoneLoan system so far.

According to him, this facility is available at Nepal Investment Mega Bank, Nabil Bank, Kumari Bank, Laxmi Sunrise Bank, NIC Asia Bank, Agriculture Development Bank, Machhapuchchhre Bank, Prabhu Bank, Rastriya Banijya Bank, and Citizens Bank. Additionally, loans are also being disbursed through the digital wallet eSewa using this platform.

Looking at the data from the initial days to the present, a significant amount of loans have been disbursed through PhoneLoan. So far, loans have been disbursed more than 5.50 lakh times through this platform. In terms of amount, PhoneLoan has stated that more than NPR 17 billion has been invested through PhoneLoan so far.

Who gets this facility? How is eligibility measured?

PhoneLoan is not a facility that everyone can get just by wishing for it. For this, the customer must have a good banking transaction track record. Natural individuals with regular income appearing in their bank accounts are the main target group.

Banks and financial institutions prioritize customers, especially those with regular salary accounts (payroll) or other sources of regular income like house rent. Sigdel states that PhoneLoan performs data analysis based on the priority criteria set by the banks.

'The main basis for identifying a customer's source of income is their bank account transactions,' Sigdel says. 'Our Decision Analytics Engine meticulously analyzes the customer's transactions for the last 12 months. Our artificial intelligence system easily detects whether the money coming into the account is a genuine salary or a fund transfer from elsewhere.'

The system determines the final loan limit only after analyzing several parameters such as the customer's income, spending patterns, account balance, and transaction trends.

Currently, when combining the data from all banks, more than approximately 5 lakh customers are in a pre-approved state, meaning they are eligible for a loan and can get an instant loan by opening their mobile banking app at any time if they wish, PhoneLoan has stated.

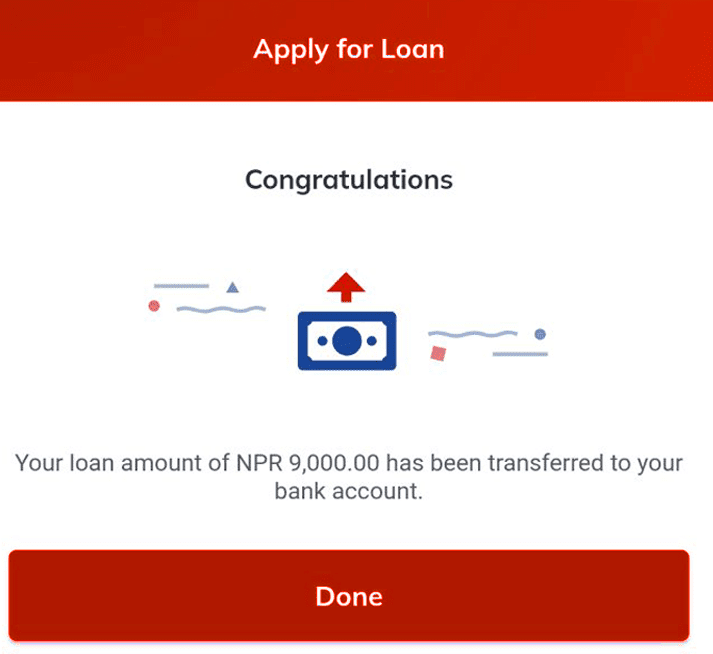

Application in Minutes, Money in Account Instantly

Customers do not need to apply anywhere to get a PhoneLoan. Sigdel explains that if a customer is eligible for PhoneLoan and their bank provides the PhoneLoan facility, a notification or icon saying 'PhoneLoan Ready' will automatically appear in their mobile banking application.

'If you see the PhoneLoan icon in your mobile banking, you should understand that you are eligible. If you are taking a loan for the first time, you need to register by providing your email ID. Then, by clicking on 'Apply Now', you need to select the amount and tenure you need within your approved limit.'

After this, the system will automatically display the applicable interest rate, processing fee, and monthly installment on the screen. As soon as you agree to all the terms, click on 'I Agree', and enter your mobile banking transaction PIN or OTP, the loan amount will be credited to the customer's account within seconds.

Interest Only on What You Use

Recently, PhoneLoan has also introduced a new feature called 'Multi Disbursement' keeping customer convenience in mind. He says that customers have really liked this feature. The company has stated that this feature allows for multiple disbursements within the credit limit.

For example, if the system shows a person is eligible for a loan of NPR 1 lakh, but the customer only needs NPR 20,000 immediately, they don't have to withdraw the full lakh and pay interest.

Sigdel says, 'Previously, after withdrawing NPR 20,000, there was a compulsion to repay the previous loan to take the remaining NPR 80,000. But after the 'Multi Disbursement' feature, customers can withdraw loans multiple times as needed, such as NPR 10,000 today and NPR 15,000 tomorrow, from their NPR 1 lakh limit. You only pay interest on the amount withdrawn.'

What is the Risk of Lending Without Collateral?

What is the risk of bank money being lost when lending without collateral? This is the most pressing question. However, PhoneLoan's data shows surprising results. Even with over NPR 17 billion in loans disbursed without collateral, its non-performing loan (NPL) ratio is only 2.12 percent. This is a very satisfactory situation compared to the overall banking industry's NPL in Nepal. The main reason for such low NPL is its credit scoring.

PhoneLoan determines the customer's credit score by analyzing the customer's account transactions and payment behavior from various aspects. Based on that credit score, the customer's loan limit is determined and adjusted over time.

The main reasons behind this are strong technology and continuous monitoring of customer behavior. 'There is no physical collateral here; the customer's behavior is the collateral,' says departmental head Sigdel. 'We continuously evaluate the customer through the 'PhoneLoan Repayment Index'. The score is determined by observing the behavior before and after taking the loan. The limit of those who repay installments properly keeps increasing, while the limit of those with poor behavior decreases or is canceled.'

Sigdel states that it is extremely important for the customer to use the loan correctly and make payments on time. Otherwise, the bank can proceed with the necessary procedures for loan recovery according to prevailing rules and banking procedures.

Moreover, there is no hassle in repaying the loan under this system. On the day the loan installment is due, the bank automatically deducts the money from the customer's account. Sigdel says that customers don't have to go and pay themselves; they just need to ensure sufficient balance in their account.

If any customer delays or defaults on even a single installment, the system blacklists them. In such a situation, they are banned from using the PhoneLoan facility from all other 10 banks in the future. It is estimated that this strict policy is also why bad loans are under control.

How is PhoneLoan Different from a Credit Card?

Many might think that similar loans are also available through credit cards. So, how is PhoneLoan different? However, Sigdel states that its concept is more detailed and comprehensive than that of a credit card.

According to him, the purpose and nature of credit cards and PhoneLoans are different. 'Credit cards are mainly used for swiping when purchasing goods at stores or merchants. But PhoneLoan is a facility where cash comes directly into your bank account. Suppose someone suddenly falls ill or needs emergency cash at home; a credit card swipe won't help in such a situation; PhoneLoan provides great relief then.'

In terms of interest rates, PhoneLoan is also cheaper than credit cards. While credit cards can typically have an interest rate of up to 2 percent per month (24 percent or more annually), banks set affordable interest rates for PhoneLoans, similar to home loans or auto loans. Currently, such interest rates are set from single digits to 14-15 percent based on the bank's base rate.

Since the interest rate varies by bank, customers also have the freedom to choose the bank offering the lowest interest rate if they are eligible with more than one bank.

PhoneLoan of Up to NPR 10 Lakhs Coming for Small Businesses

PhoneLoan, which has been providing loans of up to NPR 5 lakhs to individual consumers so far, is now preparing to expand its scope by targeting small and medium-sized businesses.

Nepal Rastra Bank has recently issued a circular allowing digital lending of up to NPR 10 lakhs for small and micro businesses. PhoneLoan is in the final stages of preparing to launch a new product for MSMEs based on this.

'Currently, PhoneLoan is used to meet personal needs. Now we are working on a model to provide business loans of up to NPR 10 lakhs to small businesses. This will provide great relief to small entrepreneurs doing business of NPR 25-30 lakhs,' Sigdel shared his future plans.

Contribution to Expanding Financial Access and Capital Formation

PhoneLoan has not only made people's daily lives easier but has also played a significant role in financial literacy and building credit history, the company claims.

Department Head Sigdel says, 'Today, whoever takes a PhoneLoan of NPR 50,000 or 1 lakh and honestly repays the installments on time is building a good credit score in the system. Tomorrow, when they become entrepreneurs or do large-scale business, this record of good behavior will provide them with the biggest basis for taking a loan of NPR 50 lakhs or 1 crore from the bank.'

This specific news has been automatically translated by AI. As a result, there may be some inaccuracies or language errors.