Government Revises Economic Bill Amidst Significant Changes

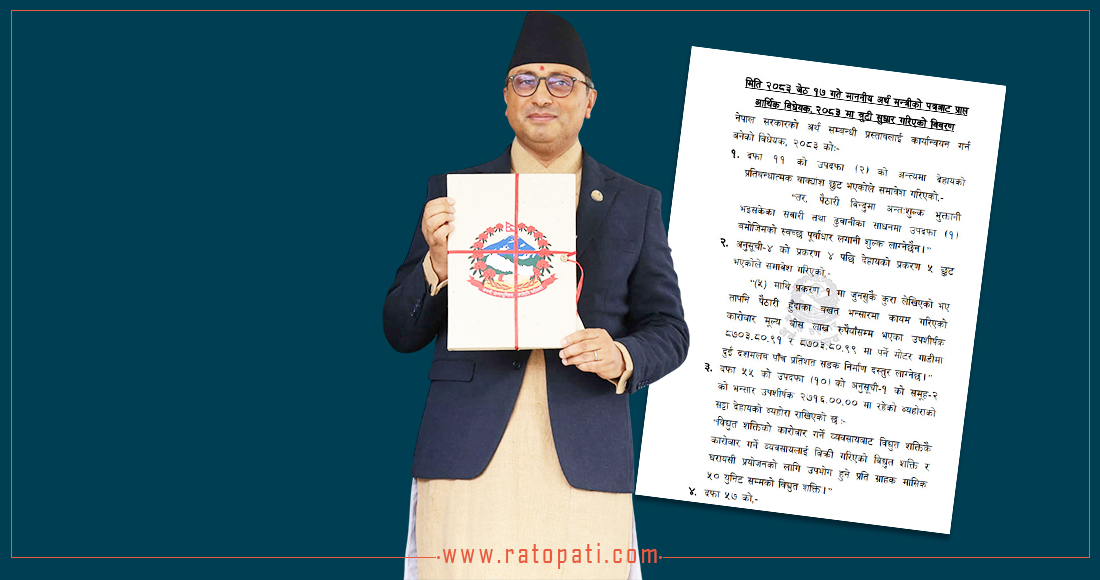

Kathmandu. The economic bill associated with the government's budget for the fiscal year 2083/084 is currently a subject of widespread discussion. A difference of 20 pages is observed between the economic bill on the Parliament's website and the one on the Ministry of Finance's website. The number of pages in the bill, which the Ministry of Finance has been updating, has been progressively decreasing.

In most other bills presented in Parliament, minor errors made by the government are not considered significant as Parliament and parliamentary committees make necessary amendments before passing them. Therefore, more attention is paid to the government's underlying objectives in the law brought through the bill, rather than literal errors.

However, the economic bill is different. Such bills are implemented immediately and contain sensitive tax-related matters, hence they are considered sensitive. Finance Minister Swarnim Wagle has also faced criticism for repeated amendments to this bill.

Nevertheless, the government has now released a bill that is 20 pages shorter, addressing the initial ambiguities and errors. However, the House of Representatives has separately registered this as an error. Here, we will list the changes made in the revised bill and their potential impact.

What were the initial provisions and what has changed?

1. Tax on Ride Sharing

- Initial Provision: The initial bill included a provision to impose VAT on ride-sharing services. However, the legal basis for this was unclear.

- Provision after revision: By adding sub-section (1b) to Section 55, it was clarified that a 5% VAT would be levied on the amount collected from passengers by 'resident ride-sharing operators'.

- Impact: The confusion among passengers using services like Pathao and inDrive about whether a 13% VAT would be applied seems to have ended.

2. VAT on Electricity Tariff

- Initial Provision: Electricity was listed under VAT exemption in one place and subject to a 5% tax in another, implying that VAT would be applied to all electricity.

- Provision after revision: It was clarified that VAT would be fully exempted for domestic consumers using up to 50 units of electricity per month and for transactions between electricity trading companies.

- Impact: Low-electricity consuming low-income and middle-class families will not face a tax burden. It is also clear that there will be no double taxation hassle in electricity trading.

3. Income Tax Exemption on Children's Education Expenses

- Initial Provision: No such provision was mentioned in the initial draft.

- Provision after revision: By amending Schedule-1 of the Income Tax Act, a provision was added allowing individuals to deduct 25% of the annual fees paid for their children's education, or a maximum of Rs 25,000, whichever is less, from their taxable income.

- Impact: Middle-class parents will receive relief on their income tax for fees paid for their children's education. However, it appears that only a very small number of families will be able to benefit from this.

4. Road Fee on Small Electric Vehicles

- Initial Provision: The rate of road construction fee on electric vehicles was high and in a single category.

- Provision after revision: A new clause was added to Schedule-4, stipulating that for small electric motor vehicles with a customs value of up to Rs 2 million, the road construction fee would be only 2.5%.

- Impact: Ordinary people purchasing cheaper and smaller electric vehicles will get price relief. The possibility of price increases is reduced.

5. Road Fee on Small Electric Vehicles

- Initial Provision: The rate of road construction fee on electric vehicles was high and in a single category.

- Provision after revision: A new clause was added to Schedule-4, stipulating that for small electric motor vehicles with a customs value of up to Rs 2 million, the road construction fee would be only 2.5%.

- Impact: Ordinary people purchasing cheaper and smaller electric vehicles will get price relief. The possibility of price increases is reduced.

6. Determination of Fee for Vehicles Between 2 to 3 Million

- Initial Provision: Previously, there was no clean infrastructure investment fee determined for vehicles between 2 to 3 million. This was a serious error.

- Provision after revision: A clean infrastructure investment fee has also been determined for this category.

- Impact: The initial error has been corrected.

7. Increase in Customs Duty on Imported Suitcases and Bags

- Initial Provision: A customs duty of 15% was proposed on suitcases and travel bags (sub-heading 4202.12.90).

- Provision after revision: This was corrected and the customs rate was increased to 30%.

- Impact: Expensive branded bags and suitcases imported from abroad will become more expensive. This will protect domestically produced similar items.

8. Capital Gains Tax on Land Acquisition

- Initial Provision: There was no clear explanation regarding the tax on gains from land acquisition.

- Provision after revision: It was clarified that a capital gains tax of only 2.5% would be levied on the compensation received by landowners in case of involuntary acquisition by government decision.

- Impact: The tax burden on citizens who have to give up land for government development projects will be reduced.

9. Strictness on Track and Trace (Digital Sticker)

- Initial Provision: Provisions for controlling revenue leakage were general.

- Provision after revision: A strict provision was added, imposing a fine of up to Rs 500,000 for unauthorized access to the track and trace system software or for tampering with data, introduced to prevent illegal trade of alcohol and tobacco.

- Impact: The scope of action against major industrialists involved in revenue evasion has been strengthened.

This specific news has been automatically translated by AI. As a result, there may be some inaccuracies or language errors.